There’s a guy in town who can dominate your life…and his name is FICO.

I’m sure most of you know, but your Fico score is basically a number that companies, creditors, etc use to calculate whether you’re a good applicant or a bad risk. Fico scores range from 350 to 850. Anything above 700 is considered excellent credit.

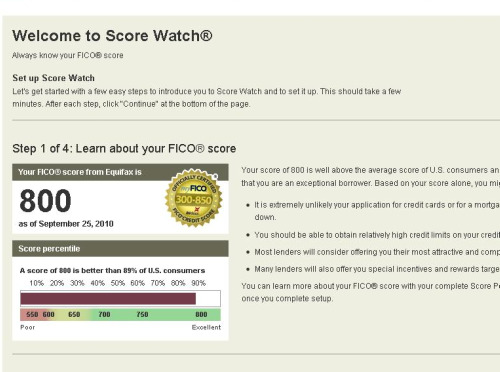

So imagine my utter happiness when I signed up at myfico.com for a free trial and found out my score is 800. Here’s the screenshot proof that I am a BAD ASS.

{kind=link}

Did you see that? I am well above the average consumer, I have excellent credit, lenders love me and life is a big fat ball of rainbows and butterflies.

But wait–this is you talking, by the way–you have credit card debt, and loans, how can you possibly have such good credit??

There are a number of factors that play into your credit score–with the number one being making all your payments on time.

- I’ve never made a late payment. Not once. Not ever.

- I’ve had a credit card since I was 14, so my credit history is at least 12 years long.

- I have a car loan, which my dad (also 800+ credit score) co-signed for me, and which I’ve paid on time, every month.

- After I got married, I called my credit cards and asked them to raise my credit balance and lower my interest rate.

Okay, okay, sorry Erika we’re not as anal responsible as you–this is still you talking, by the way–I made some mistakes when I was younger, what can I do to improve my score now?

I also checked Eric’s score to see where we stood together. Now that we’re married, lenders will look at both our scores if we apply for a loan together.

Eric’s score of 684 is listed as “good”, but not “very good” and it is a little below the national average. If you can see on the right, his credit history is not very long and that’s what’s hurting him the most. Since he doesn’t have any car loans or student loans (lucky guy), the only thing against him is his credit card debt, which we transferred to a joint credit card when we got married with a special 0% interest rate through April 2011. (another reason to get rid of the debt by then!)

He made two late payments which didn’t hurt him significantly, but put him in the “very good” not “great” category. Although, now that I’m handling the budget, you can bet that will never happen again. And his amount of new credit is also “very good,” not “great.”

We want to up Eric’s score, and the best bet right now, would be to increase his credit line, thereby increasing his debt to credit ratio. The higher credit he has, the less debt it appears he has.

For example, before I got married, one of my my credit cards had a $5,000 limit. Just by calling, I was able to up it to $10,000 and reduce my interest rate as well. There for, instead of having $3700 debt to a $5,000 line (74% debt!), it appears we have $3700 to $10,000 (37%). We actually have more credit line than that, but you get the picture.

Also–Eric had some pretty bad credit cards. One of them had an annual fee! Why on earth would anyone sign up for an annual fee credit card these days when you get free ones that offer you rewards? We got rid of that one pronto! Normally, I wouldn’t advise on closing credit cards unless they’re really bad, like this one was.

The great thing about this free trial on myfico.com (btw, I’m not getting paid to write about this) is that you can also see how your FICO score can improve with changes! If we make all our payments on time for the next 12 months, Eric’s score will improve to between 704-734. That means he’ll go from the “good” category to “Excellent” category in ONE YEAR!

Other tips:

- Don’t open too many credit cards at once.

- Continue to make payments on time, even the minimum balance!

So there you have it! Our Fico Score! Hopefully, we won’t have to use it for a while, but it’s always good to do an annual check on your score and credit history to make sure nothing is amiss.

Any tips on improving your score? Any FICO happy stories out there? Anyone willing to share their FICO?

13 comments

Very good article, we must realize that the lender is somehow on the opposite side of us. They have an interest in the welfare of their company. Perhaps having a high FICO value is quite proud, but on the one hand we have become a very remarkable object of their benefit by providing a huge income for creditors for years.

It is not my first time to visit this web page, i am visiting this web

page dailly and obtain fastidious facts from here

all the time.

[…] wasn’t surprised when I found out I qualified for an excellent credit score. I opened my first credit card at 14 with a $500 limit, and this helped to establish a long credit […]

You could definitely see your expertise within the article

you write. The world hopes for more passionate writers like you who are not afraid to mention

how they believe. Always go after your heart.

Hey! I’m a little late to this post, but I’m enjoying reading through everything. I was wondering how you went about combining credit card debt into a no-interest one? We do pretty well making payments on our cards, but if we even got just a little break in all the INTEREST we would be sitting very nicely. Thanks!

Ugh, I know far too much about credit scores… and not because I have a good one! I had admitting that, but it was the one thing that went down the tubes with the ex. One would think that when I found out his score was somewhere in the low 400’s, I would have taken it to be a sign that he was not that responsible… but apparently I was very naive and whenever he wanted something, I co-signed (stupid, stupid, stupid!!) and then guess who never paid a dime when we split?

I really wish I could have found a way to pay it all without getting behind but I was only one income. This is why I want my finances, debt, and assets separate in the future. Luckily though, I’ve been working hard at improving my score again, and it’s looking a lot better than it used to.

Wow… mine is 558. Which I figures should be good, but apparently it is not. Oh well, I can only do my best to fix that and it will probably take me a while to do that. I find your blog very inspiring… even though I am single at this point in time.

I would love it if you would provide an easy way for me to follow you!

I worked hard to get excellent credit, and it certainly helped when my husband and I bought our house. Just one less thing to think about. We sat down, the loan officer said “credit, excellent, moving on.” Which was such a relief!

It’s amazing how “easy” it is to get great credit if you just play the system right. Which isn’t to say that having good credit is easy, it takes work. But like any other rating system, once you figure out how to play, it’s not so challenging!

Woaw…. A bad ass you are! If your score gets any higher, you might not fit into some of the ranking meters, I too should check mine out. Though I’m scared to see what years of my shopping addictions might have done to it, eek!

Also, is there a way to follow your blog? I can’t seem to find the way to do it. Help?

The number: 775. I also have a spotless record and pay off my credit cards in full every month, so your 800 is outstanding. You are a bad-ass!

When your myfico.com trial is over, you can continue to monitor your credit for free at creditkarma.com.

Good luck!

Ok, so maybe I shouldn’t have looked mine up? Or maybe I should have? Regardless, it’s not that great. It’s not terrible though. I guess I should really buckle down and get those credit cards paid off. Yowzers!

I just went and was sad that I only have 736. Unfortunately our stupid credit cards are apparently out of control and that is the only real ding on my report. I love the simulator and checking out different scenarios. By paying down that debt it’ll shoot my score up to 800. Now I just have to check out husbands score….

You are brave people for putting your credit scores out there like that! I guess I should man-up and put ours out there…..

Brandt – 750

Ashley – 780

I knew my credit score when I was in school, and my wife has never had credit cards (thus no need to know her credit score), but when we started going through the process to get pre-approved for a loan, my loan officer was falling off her seat at our credit score (no CC debt, no student loans, on time every month, the only thing that hurt us was lack of credit history).

On time payments, I’ve learned, is the biggest thing. I didn’t know about upping your credit limit – we’ve been at the same introductory $500,00 limit since we got the card, and I’ve never felt the need to up it. Maybe I should?